Tech Pique (24 June)

Staying Rationale

Fred Wilson wrote a post about Staying Positive at a time when much of what is happening in the early stage and tech sector is not. It resonated. It’s important to retain a balanced perspective during these extreme times. Everything in the media is designed to get clicks so naturally stories about Voly reducing it’s workforce (more here) get the headlines today. Equally, during the good times, the media latched on to every raise, discussing innovation and fueled the hype around the sector.

It’s important to stay rationale, in good times and bad.

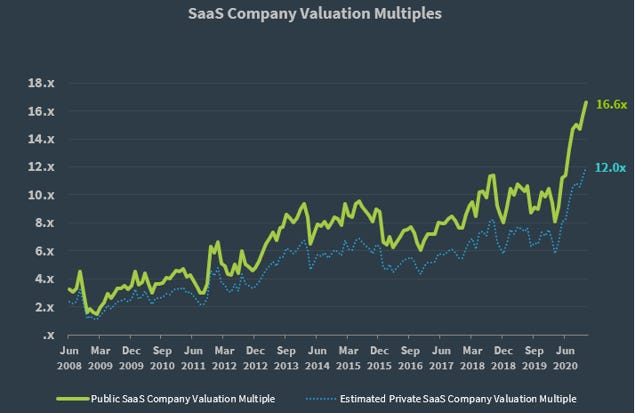

As I prepare to present at the UNSW Angel Investor Program next Thursday about Valuations and Portfolio Construction, I looked back at my slides from last year’s Program and the chart that talks to SAAS valuations.

Valuations were increasing and it was common in 2021 for early stage companies to be raising at 20x annual recurring revenue (ARR) and we even saw $100m post-money valuations for seed stage raises in the US.

My strapline to the slide was “Generally early Stage SAAS companies are valued at 6-8x TTM / current recurring revenue”.

It was clear to me, and a few others in the space that I was speaking to, that valuations had become frothy. The reason that 6-8x recurring revenue makes sense is because this is more-or-less the historical average / median. There will always be company specific factors that make companies raise at more or less than average which need to be taken into account as well.

When companies raise at 20x ARR and the market multiple reverts to 8x, revenue needs to grow 2.5x to justify the last round’s valuation…and if you’re raising at this valuation, it’s effectively a down round. To give investors a great return between rounds, revenue would have to grow 5x so that the valuation doubles. The trouble is most companies weren’t funded well enought to grow 5x.

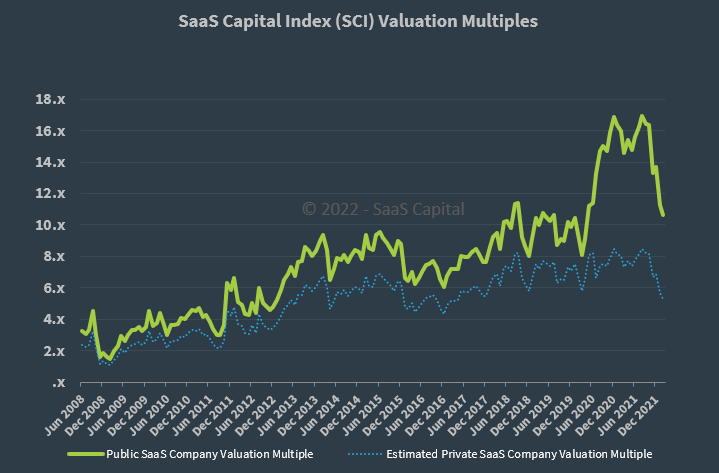

As we look at the updated version of the graph above, we see that valuations have fallen below 6x (for private companies).

I still think 6-8x recurring revenue makes sense as an entry valuation. Investors should be thinking about holding for 5-7 years, especially at in priavte market at early stage and I’m a believer in generating investment returns through creating additional value (i.e. revenue) not multiple arbitrage.

So to investors, while the market is down, I don’t think you should be squeezing founders and aggressively diluting them to get a slightly better deal. I don’t think that’s in the long-term benefit of the company as it doesn’t align founders and investors.

To founders, there’s still capital out there and investments are getting made - yes, investors are taking longer, doing more DD and not funding companies at 20x ARR but they are making investments. It’s even more crucial today to find the right long term investment partner for your business; a great signal for this is how they act in respect to entry valuation and dilution.

Stay rationale (& positive).